July 2017

A New Climate for Change

Max Cappetta, CEO, Redpoint Investment Management

"This one trend, climate change, affects all trends." Barack Obama 2015 UN Climate Change Conference – Paris

There is arguably no greater investment challenge today than the impact of climate change. Since the first Intergovernmental Panel on Climate Change (IPCC) Assessment report in 1990 the issue of greenhouse gas (GHG) emissions has evolved from a government reporting matter to recognition of climate change as a key investment risk. The investment challenge of climate risk is multi-faceted: starting from an assessment of the carbon intensity of a business through to the uncertainty of the timing and mechanism by which GHG emissions become priced and ultimately impact asset values.

Stranded Assets

The concept of a “stranded asset” is not new. Historical examples include the transition from fixed line to mobile phones and from cellulose film to digital cameras. At present, companies that own fossil fuel deposits may face a similar demise based on either government imposed extraction quotas or competitive and technological substitution by companies who utilise such fuels as inputs.

The identification of assets with the potential to be stranded by the policy and/or competitive forces of climate change is complex but achievable. Coal mines and mines owning utilities are such examples. So, to more accurately and effectively reduce a portfolio’s exposure to carbon risk, deeper analysis is required.

Assessing carbon intensity

UK based advisory firm Trucost has been assessing the economic impact of the dependence that companies have on natural resources for over a decade. Their approach, in relation to the GHG emissions of companies, is to consider them in three (3) broad categories: [1]

- Scope 1 emissions: direct GHG emissions from sources owned or directly;

- Scope 2 emissions: indirect GHG emissions resulting from consumption of electricity, heat or steam; and

- Scope 3 emissions: all other indirect GHG emissions excluding Scope 2 caused by the business but released from sources not owned or controlled by the company.

Carbon Intensity for each company is calculated as metric tonnes of GHG emissions (in carbon dioxide equivalents – CO2e) divided by company revenue in millions of US dollars.Scope 1 and Scope 2 data are required to be reported by companies if they are to comply with the GHG Protocol corporate reporting standard. [1] Scope 3 reporting is an optional disclosure. Given the high level of company compliance with the standard, Scope 1 and Scope 2 data is used by some vendors to calculate carbon intensity.

Trucost’s preferred measure extends to incorporate Scope 3. These Scope 3 emissions are those from direct service providers within a company’s supply chain. The justification for this extension is to ensure a more accurate comparison between companies with similar activities underpinning their outputs, but with different degrees of outsourcing.

What’s the difference?

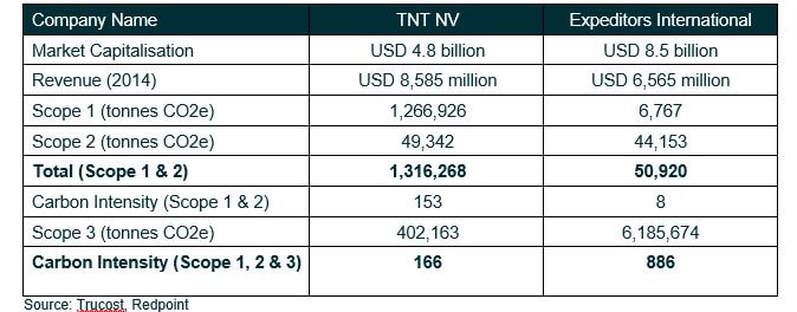

The definitional differences between Trucost’s carbon intensity estimates and Scope 1 and Scope 2 carbon intensity estimates can be highlighted by comparing two (2) similar companies: delivery specialists TNT NV and Expeditors International.

The table highlights that quite different conclusions can be drawn based on the carbon intensity measure being used. Using only Scope 1 and Scope 2 data, Expeditors International appears to have significantly lower carbon intensity than TNT NV. However, incorporating first tier indirect emissions from suppliers reveals that Expeditors International has vastly higher carbon intensity. This impact is due to Expeditors International’s specific business model of being a non-asset holding global logistics provider: they outsource their transportation needs via other businesses. This example highlights how the assessment of two (2) companies in the same business can vary significantly with the choice of carbon intensity measure.

This depth of analysis and insight will become more important for investors as they seek to understand their investments in the context of climate change risk. While a review of stranded assets is a useful starting point there is likely to be merit in considering deeper insights into the carbon intensity of individual companies. This greater detail will assist innovative investors to make improved risk and return trade-offs that more effectively capture this important social and financial risk.

This depth of analysis and insight will become more important for investors as they seek to understand their investments in the context of climate change risk. While a review of stranded assets is a useful starting point there is likely to be merit in considering deeper insights into the carbon intensity of individual companies. This greater detail will assist innovative investors to make improved risk and return trade-offs that more effectively capture this important social and financial risk.

Footnotes

[1] The latest carbon footprint data is sourced from Trucost, which maintains the world’s largest database of greenhouse gas (GHG) disclosures. See http://www.trucost.com/ for further details.

[2] The Greenhouse Gas (GHG) Protocol, developed by World Resources Institute (WRI) and World Business Council on Sustainable Development (WBCSD), sets the global standard for how to measure, manage, and report greenhouse gas emissions.

[1] The latest carbon footprint data is sourced from Trucost, which maintains the world’s largest database of greenhouse gas (GHG) disclosures. See http://www.trucost.com/ for further details.

[2] The Greenhouse Gas (GHG) Protocol, developed by World Resources Institute (WRI) and World Business Council on Sustainable Development (WBCSD), sets the global standard for how to measure, manage, and report greenhouse gas emissions.

Important information : This communication is provided by Redpoint Investment Management Pty Limited (ABN 83 152 313 758, AFSL 411671) (Redpoint). The information in the communication is of a general nature only and is not financial product advice. The communication is not intended to offer products or services provided by Redpoint or its affiliates. Opinions constitute our judgement at the time of issue and are subject to change. Neither Redpoint nor its employees or directors give any warranty of accuracy or reliability, nor accept any responsibility for errors or omissions in this communication.