About redpoint

redpoint Investment Management is a boutique fund manager based in Sydney. We specialise in listed asset classes including Australian equities, international equities, global infrastructure and global property.

We use our extensive quantitative skills, acute understanding of risk management, and trade-implementation capabilities to design and create investment solutions to meet our clients’ needs and objectives.

redpoint is majority staff owned, with GSFM Pty Ltd (a CI Financial company), holding a minority share. As such, we combine the strength of GSFM’s dedicated distribution capability and CI’s global backing with our skills to be a highly focused and specialist equities manager. As a largely employee-owned boutique, our interests are closely aligned with those of our clients, and we have the strength and expertise to deliver better investment outcomes.

Our disciplined process means we take the emotion out of investing – we see opportunities to add value within markets and capture these opportunities through:

We use our extensive quantitative skills, acute understanding of risk management, and trade-implementation capabilities to design and create investment solutions to meet our clients’ needs and objectives.

redpoint is majority staff owned, with GSFM Pty Ltd (a CI Financial company), holding a minority share. As such, we combine the strength of GSFM’s dedicated distribution capability and CI’s global backing with our skills to be a highly focused and specialist equities manager. As a largely employee-owned boutique, our interests are closely aligned with those of our clients, and we have the strength and expertise to deliver better investment outcomes.

Our disciplined process means we take the emotion out of investing – we see opportunities to add value within markets and capture these opportunities through:

- investment insights, robustly researched

- risk focused portfolio construction; and

- efficient execution.

Investment Philosophy

While we believe that financial markets are broadly efficient, opportunities to add value still exist by skilfully exploiting various rewarded risk premia and return anomalies caused by investor behavioural biases. These opportunities manifest over various time frames spanning longer-term signals (such as valuation and sustainable company quality), medium term signals (such as analyst sentiment), and short-term signals (incorporating price movements and company news flow).

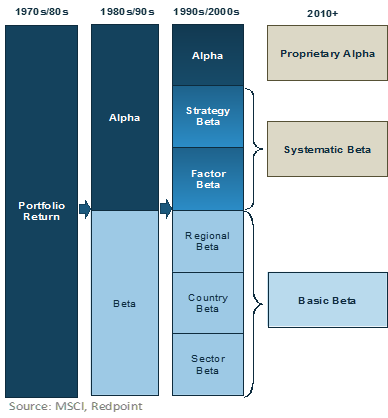

The evolution of return attribution over time, as described in this chart, has shown that outperformance can be decomposed into different components. The systematic elements are those that can be easily replicated with simple approaches (e.g. buy low P/E stocks to capture a value risk premium).

Our stock selection signals (alpha drivers) borrow from systematic beta strategies in that they are disciplined quantitative encapsulations of a fundamental investment insight. We seek to capture elements of proprietary alpha through more detailed analysis and sophisticated decision rules delivered via robust research and our team’s global investment management experience.

Our stock selection signals (alpha drivers) are founded on fundamentally based investment insights, complemented with a large body of academic research that highlights human behavioural biases creating persistent mispricing opportunities and a growing body of work supporting the incorporation of environmental, social and corporate governance (ESG) considerations. We believe that the incorporation of ESG issues can add value for clients and, consequently, all our strategies integrate

and / or screen on ESG considerations. We incorporate ESG issues into all active strategies where we have full discretion and encourage incorporation where the client limits that discretion.

Combining these complementary and nuanced signals through robust portfolio construction techniques and efficient implementation leads to better risk-adjusted return outcomes in the long term.

Our investment team have been managing systematic Australian and global equity strategies for over 20 years. This experience is critical to delivering better investment outcomes through a deep understanding of the specific nature of the equity markets and the risk / return characteristics of systematic quantitative equity strategies.

While we believe that financial markets are broadly efficient, opportunities to add value still exist by skilfully exploiting various rewarded risk premia and return anomalies caused by investor behavioural biases. These opportunities manifest over various time frames spanning longer-term signals (such as valuation and sustainable company quality), medium term signals (such as analyst sentiment), and short-term signals (incorporating price movements and company news flow).

The evolution of return attribution over time, as described in this chart, has shown that outperformance can be decomposed into different components. The systematic elements are those that can be easily replicated with simple approaches (e.g. buy low P/E stocks to capture a value risk premium).

Our stock selection signals (alpha drivers) borrow from systematic beta strategies in that they are disciplined quantitative encapsulations of a fundamental investment insight. We seek to capture elements of proprietary alpha through more detailed analysis and sophisticated decision rules delivered via robust research and our team’s global investment management experience.

Our stock selection signals (alpha drivers) are founded on fundamentally based investment insights, complemented with a large body of academic research that highlights human behavioural biases creating persistent mispricing opportunities and a growing body of work supporting the incorporation of environmental, social and corporate governance (ESG) considerations. We believe that the incorporation of ESG issues can add value for clients and, consequently, all our strategies integrate

and / or screen on ESG considerations. We incorporate ESG issues into all active strategies where we have full discretion and encourage incorporation where the client limits that discretion.

Combining these complementary and nuanced signals through robust portfolio construction techniques and efficient implementation leads to better risk-adjusted return outcomes in the long term.

Our investment team have been managing systematic Australian and global equity strategies for over 20 years. This experience is critical to delivering better investment outcomes through a deep understanding of the specific nature of the equity markets and the risk / return characteristics of systematic quantitative equity strategies.

The term ‘redpoint’ is associated with climbing. To redpoint a climb is to successfully lead a climb without stopping or resting on your ropes. Success in climbing requires many skills including stamina, strength, knowledge and confidence. Climbing is an inherently dangerous sport and experience is critical to properly assess risk and make the right decisions. The redpoint ethos is to be a trusted partner and investment guide for clients. redpoint uses the best ideas from its investment team along with ongoing research to deliver a range of scalable, flexible and enduring outcomes from listed equity investing.