March 2020

Global listed infrastructure benchmarking in a Your Future, Your Super world

Ganesh Suntharam, Chief Investment Officer, redpoint Investment Management

Overview

The proposed ‘Your Future, Your Super’ (YFYS) legislation has brought benchmark selection within superannuation products into greater focus. In this note, we look at common benchmarks used for managing the global listed infrastructure component of superannuation options. We find that the varied nature of benchmark rules and construction methodologies results in differing risk and performance characteristics of these commonly used benchmarks.

The implication of our findings is that managers of superannuation assets will need to assess their risk tolerance levels, and potentially incorporate an element of risk control, in the construction of their member portfolios.

Exposure of benchmarks to infrastructure subsectors

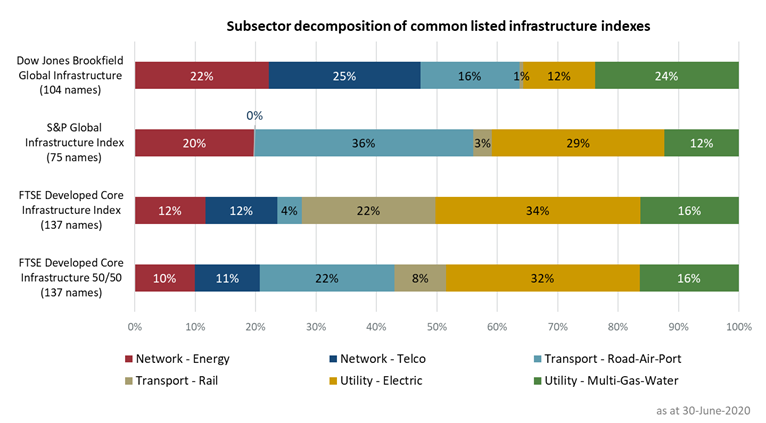

When it comes to listed infrastructure, index vendors can have unusually differing definitions of what constitutes an infrastructure company. This differing definition at a constituent level coupled with varying index construction rules can lead to significantly different exposures at the aggregate index level. The following diagram highlights the variations in subsector exposure due to different index construction rules for four commonly referenced infrastructure benchmarks.

The proposed ‘Your Future, Your Super’ (YFYS) legislation has brought benchmark selection within superannuation products into greater focus. In this note, we look at common benchmarks used for managing the global listed infrastructure component of superannuation options. We find that the varied nature of benchmark rules and construction methodologies results in differing risk and performance characteristics of these commonly used benchmarks.

The implication of our findings is that managers of superannuation assets will need to assess their risk tolerance levels, and potentially incorporate an element of risk control, in the construction of their member portfolios.

Exposure of benchmarks to infrastructure subsectors

When it comes to listed infrastructure, index vendors can have unusually differing definitions of what constitutes an infrastructure company. This differing definition at a constituent level coupled with varying index construction rules can lead to significantly different exposures at the aggregate index level. The following diagram highlights the variations in subsector exposure due to different index construction rules for four commonly referenced infrastructure benchmarks.

Source : Redpoint, Axioma

The above diagram shows that index rules around the inclusion/exclusion of rail transport and telecommunication infrastructure assets, as well as additional rules to further emphasise non-rail transportation assets in some indexes, yields quite different subsector exposures (even when the index is produced by the same index vendor).

Although the subsector differences presented were for four commonly available indexes, it is worth noting that traditional active managers in the listed infrastructure space can also have quite divergent investment approaches. In many instances, a best ideas portfolio holding twenty or thirty names can also vary quite considerably from the index it is benchmarked to and will likely exhibit greater stock specific risk due to the concentrated nature of its holdings[1].

Historical performance and risk of infrastructure benchmarks

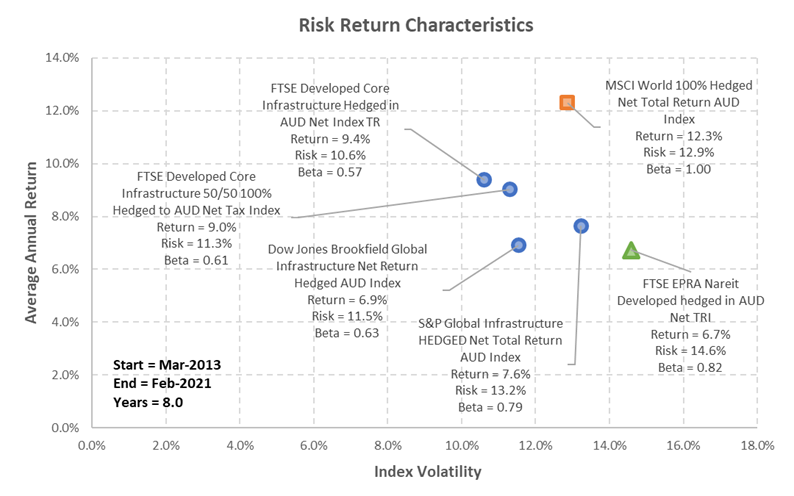

Differences in index construction methodologies highlighted in the previous section of this document leads to variations in the risk and return characteristics of each benchmark. The following figure presents the risk and return characteristics of the four commonly used infrastructure benchmarks along with a global equity and global listed property index over an 8-year period from Mar-2013 to Feb-2021. This horizon was chosen to align with the current performance measurement period proposed in the YFYS legislation.

Although the subsector differences presented were for four commonly available indexes, it is worth noting that traditional active managers in the listed infrastructure space can also have quite divergent investment approaches. In many instances, a best ideas portfolio holding twenty or thirty names can also vary quite considerably from the index it is benchmarked to and will likely exhibit greater stock specific risk due to the concentrated nature of its holdings[1].

Historical performance and risk of infrastructure benchmarks

Differences in index construction methodologies highlighted in the previous section of this document leads to variations in the risk and return characteristics of each benchmark. The following figure presents the risk and return characteristics of the four commonly used infrastructure benchmarks along with a global equity and global listed property index over an 8-year period from Mar-2013 to Feb-2021. This horizon was chosen to align with the current performance measurement period proposed in the YFYS legislation.

Source : Redpoint, Bloomberg

In the context of an asset allocation process, the four infrastructure benchmarks have some similarities: they mostly have a lower volatility than a traditional global equity index and with a beta between 0.55 and 0.80 relative to global equities which is in keeping with investor expectations.

However, looking within the asset class, the four infrastructure benchmarks do generate quite different historical return profiles. These performance differences can also shift considerably based on the time period of analysis[2]. To set aside the discussion on the impact of the measurement time horizon (which has been a contentious point in YFYS feedback), we instead review the relative risk metrics of the four benchmarks in greater detail.

Relative risk characteristics infrastructure benchmarks

The current YFYS legislation has marked the FTSE Developed Core Infrastructure Index as the relevant benchmark for assessing relative performance of infrastructure options within a superannuation pool. Using this prescribed index as the reference, we compare the three other indexes in a relative sense in order to assess the risk introduced by making an active decision to move away from this YSYF prescribed benchmark.

However, looking within the asset class, the four infrastructure benchmarks do generate quite different historical return profiles. These performance differences can also shift considerably based on the time period of analysis[2]. To set aside the discussion on the impact of the measurement time horizon (which has been a contentious point in YFYS feedback), we instead review the relative risk metrics of the four benchmarks in greater detail.

Relative risk characteristics infrastructure benchmarks

The current YFYS legislation has marked the FTSE Developed Core Infrastructure Index as the relevant benchmark for assessing relative performance of infrastructure options within a superannuation pool. Using this prescribed index as the reference, we compare the three other indexes in a relative sense in order to assess the risk introduced by making an active decision to move away from this YSYF prescribed benchmark.

Source : Redpoint, Axioma

The above table presents the tracking error of the three infrastructure indexes relative to the FTSE Core benchmark. These calculations are made over a 15+ year period from Jan-2006 to Feb-2021 and the observed tracking errors highlight the that the relative variations in monthly returns can be quite significant.

Within the FTSE family, the two FTSE indexes have a tracking error of just under 3% relative to each other. Assessing the FTSE Core Index against the S&P and Dow Jones indexes results in tracking errors of 5.85% and 4.62% respectively. Traditional concentrated managers in the infrastructure space can also have a considerably higher tracking error relative to the FTSE Core benchmark. Hence, allocators impacted by this proposed legislation need to make an informed decision on how much active risk they need to deploy in order to generate the best risk-adjusted returns for their members.

Redpoint’s approach to infrastructure

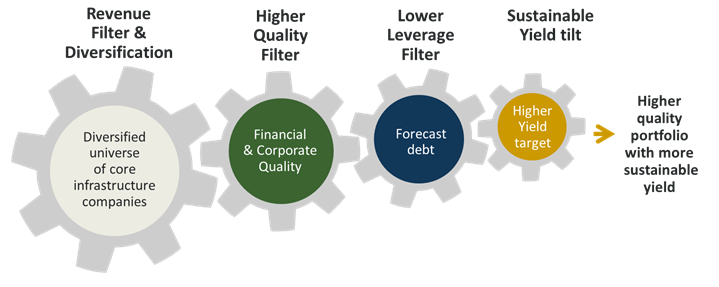

Redpoint’s approach aims to maximise risk-adjusted return from a diversified portfolio of global listed infrastructure securities. Given the noticeable differences in index vendor and manager approaches in this space, Redpoint's approach starts by creating a Strategic Reference Portfolio (SRP) that provides an internal reference index to be used in portfolio construction.

This SRP is constructed by: (a) establishing an investment universe of infrastructure securities; (b) diversifying across infrastructure subsectors to manage overall volatility; and (c) diversifying amongst individual stocks to mitigate stock concentration risk. The weighting scheme established by Redpoint’s diversification approach aims to improve the overall risk characteristics of the portfolio relative to the standard indexes presented previously.

The Redpoint approach recognises that each infrastructure subsector complements the overall outcome. However, we also recognise that each subsector has different risk characteristics that need to be weighted appropriately in order to maximise risk-adjusted return.

Hence, the strategic reference portfolio establishes the target allocation to the six infrastructure subsectors. Subsequent components of the investment process look to deviate away from the strategic reference portfolio in order to enhance financial characteristics such as yield, leverage, sustainability and other financial return drivers. A representation of the overall investment process is presented below:

Source: Redpoint

The Redpoint GLI portfolio has a realised tracking error of approximately 1.5% relative to its underlying benchmark. For background, it is worth noting that when the strategy was first launched in April 2012, the benchmark for the strategy was the FTSE Developed Core Infrastructure Index. This index was chosen after an internal review of infrastructure index vendors found that the revenue cut-offs introduced by FTSE to define ‘core’ assets were a material improvement on other available indexes in the marketplace. This definition assisted with capturing a better overall asset class exposure and was also beneficial in delivering better client outcomes.

In 2015, FTSE subsequently released 50/50 series of indexes as a targeted replacement for the UBS 50/50 index which was decommissioned by UBS due to banking regulation changes. The FTSE 50/50 index, which was gaining greater market acceptance, came with both benefits and drawbacks which required further analysis from our perspective. Redpoint completed this analysis in 2016 and, after making further adjustments to our strategic reference portfolio, we moved the GLI strategy to the FTSE Developed Core Infrastructure 50/50 index in September 2017 following a 3-month transition.

Although we have done considerable work in understanding the various infrastructure indexes, in the context of our overall investment process, the index is the starting point to our process and not the end point. Within our process, the index provides us with an important subset of core infrastructure companies which we then supplement before restructuring the constituents in order to create our preferred starting point, the SRP.

Given our approach primarily focusses on the SRP, the tracking error of the GLI strategy has remained at approximately 1.5% against both flavours of the FTSE index. This tracking error outcome is actively managed within our existing portfolio construction process by utilising a number of constraints in order to manage the overall risk characteristics of the final portfolio. We believe that risk management is an important consideration when looking to construct better risk-adjusted portfolios.

With the proposed introduction of the YFYS legislation, we have had several questions on the implications of a tighter tracking error requirement relative to the FTSE Developed Core Infrastructure Index. A key element of active risk is the subsector deviations of a portfolio relative to the underlying index. Hence, limiting the size of active sector exposure allows investors to control a critical element of risk that impacts tracking error.

Given the systematic nature of our approach and the flexibility embedded in our portfolio optimisation software, tighter risk limits can be incorporated into our investment process without compromising the philosophy and objective for our strategy. This adjustment may suit some asset owners who are revisiting their risk tolerance levels.

Implications for risk tolerance

As the discussion around ‘Your Future, Your Super’ continues to evolve, the initial question for most asset owners will be around their choice of benchmark relative to that proposed as a YFYS default. This document highlights quite varied subsector and risk characteristics for four commonly used global listed infrastructure indexes. Our analysis indicates a tracking error variation of between 2.5% and 6.0% depending on the choice of benchmark relative to that proposed in YFYS. Given this wide range of tracking errors, an initial question for asset owners will be around their risk tolerance (or appetite) in relation to benchmark selection.

Once asset owners have reviewed their selection of benchmark, a second consideration is to assess the active risk budget they are willing to deploy relative to the selected benchmark. This decision will be influenced by the investment process of their underlying managers which can also vary quite considerably from their underlying benchmarks due to the concentrated nature of many portfolios. It should be noted that stock concentration is not necessarily limited to active management. Poorly constructed benchmarks in a narrow segment of investment market are subject to similar concentration risk due to the market capitalisation weighting scheme they typically utilise.

Hence, risk tolerance (or appetite) in relation to:

will become more important considerations as asset owners look to maximise risk adjusted returns from their members’ portfolios.

[1] See the appendix of this article for risk and return characteristics of each infrastructure subsector over a 15+ year period. Index and manager allocations to each subgroup can have a material impact on the final return outcome.

[2] See appendix for the same chart presented over a 15+ year time horizon.

In 2015, FTSE subsequently released 50/50 series of indexes as a targeted replacement for the UBS 50/50 index which was decommissioned by UBS due to banking regulation changes. The FTSE 50/50 index, which was gaining greater market acceptance, came with both benefits and drawbacks which required further analysis from our perspective. Redpoint completed this analysis in 2016 and, after making further adjustments to our strategic reference portfolio, we moved the GLI strategy to the FTSE Developed Core Infrastructure 50/50 index in September 2017 following a 3-month transition.

Although we have done considerable work in understanding the various infrastructure indexes, in the context of our overall investment process, the index is the starting point to our process and not the end point. Within our process, the index provides us with an important subset of core infrastructure companies which we then supplement before restructuring the constituents in order to create our preferred starting point, the SRP.

Given our approach primarily focusses on the SRP, the tracking error of the GLI strategy has remained at approximately 1.5% against both flavours of the FTSE index. This tracking error outcome is actively managed within our existing portfolio construction process by utilising a number of constraints in order to manage the overall risk characteristics of the final portfolio. We believe that risk management is an important consideration when looking to construct better risk-adjusted portfolios.

With the proposed introduction of the YFYS legislation, we have had several questions on the implications of a tighter tracking error requirement relative to the FTSE Developed Core Infrastructure Index. A key element of active risk is the subsector deviations of a portfolio relative to the underlying index. Hence, limiting the size of active sector exposure allows investors to control a critical element of risk that impacts tracking error.

Given the systematic nature of our approach and the flexibility embedded in our portfolio optimisation software, tighter risk limits can be incorporated into our investment process without compromising the philosophy and objective for our strategy. This adjustment may suit some asset owners who are revisiting their risk tolerance levels.

Implications for risk tolerance

As the discussion around ‘Your Future, Your Super’ continues to evolve, the initial question for most asset owners will be around their choice of benchmark relative to that proposed as a YFYS default. This document highlights quite varied subsector and risk characteristics for four commonly used global listed infrastructure indexes. Our analysis indicates a tracking error variation of between 2.5% and 6.0% depending on the choice of benchmark relative to that proposed in YFYS. Given this wide range of tracking errors, an initial question for asset owners will be around their risk tolerance (or appetite) in relation to benchmark selection.

Once asset owners have reviewed their selection of benchmark, a second consideration is to assess the active risk budget they are willing to deploy relative to the selected benchmark. This decision will be influenced by the investment process of their underlying managers which can also vary quite considerably from their underlying benchmarks due to the concentrated nature of many portfolios. It should be noted that stock concentration is not necessarily limited to active management. Poorly constructed benchmarks in a narrow segment of investment market are subject to similar concentration risk due to the market capitalisation weighting scheme they typically utilise.

Hence, risk tolerance (or appetite) in relation to:

- benchmark selection relative to proposed YFYS legislation, and

- active risk budget deployed around a selected benchmark

will become more important considerations as asset owners look to maximise risk adjusted returns from their members’ portfolios.

[1] See the appendix of this article for risk and return characteristics of each infrastructure subsector over a 15+ year period. Index and manager allocations to each subgroup can have a material impact on the final return outcome.

[2] See appendix for the same chart presented over a 15+ year time horizon.

For further details please contact

Charles Levinge - Head of Institutional Business, GSFM

[email protected]

+61 3 9949 8862

+61 418 562 612

Charles Levinge - Head of Institutional Business, GSFM

[email protected]

+61 3 9949 8862

+61 418 562 612

Important information : This communication is provided by Redpoint Investment Management Pty Limited (ABN 83 152 313 758, AFSL 411671) (Redpoint). The information in the communication is of a general nature only and is not financial product advice. The communication is not intended to offer products or services provided by Redpoint or its affiliates. Opinions constitute our judgement at the time of issue and are subject to change. Neither Redpoint nor its employees or directors give any warranty of accuracy or reliability, nor accept any responsibility for errors or omissions in this communication.