December 2021

Redpoint Responsible Investment Policy

Introduction

Redpoint was founded in 2011 with the integration of Economic, Environmental, Social and Governance (EESG) issues into our portfolios as a strong founding principle. Our philosophy in relation to the integration of EESG is primarily focussed on maximising risk-adjusted returns for our clients where both the risk and return elements embed EESG considerations.

Redpoint currently manages quantitative equity portfolios across a range of equity asset classes including Australian equities, international equities, global infrastructure, and global property for both institutional and retail investors. All our portfolios currently embed elements of Sustainability by using EESG as an input into the stock selection process and/or using Socially Responsible Investing (SRI) considerations to explicitly exclude assets from our portfolios.

This document outlines our approach to Responsible Investing which utilises a systematic and repeatable framework to help clients address their commitments as universal owners of listed assets.

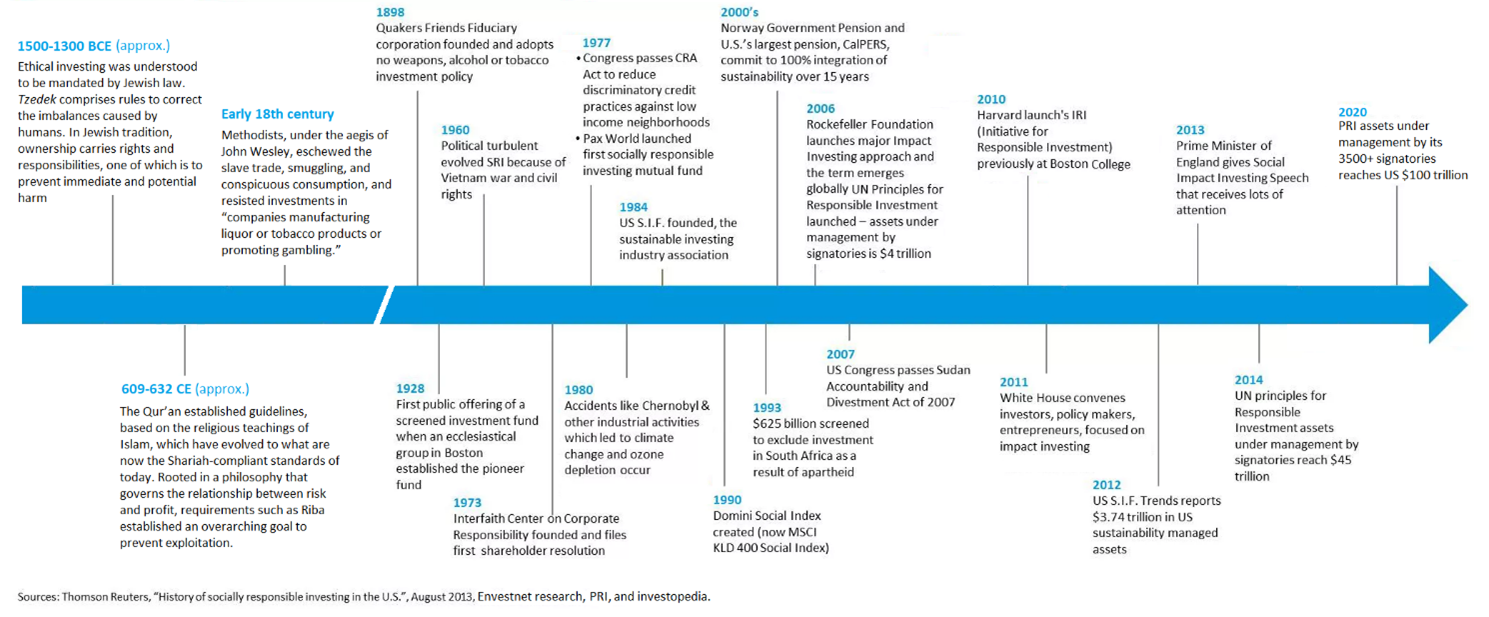

A historical perspective on socially principled investing

The more experienced investment professionals of today recall the socially driven movement advocating for the divestment of firms engaged in business in South Africa as a response to their policies around apartheid in the mid-80s and early 90s. University endowment funds were typically the first to be impacted by these protests seeking to ensure that socially principled positions, like apartheid and the Vietnam War, were reflected in their investment portfolios. But the rich history of socially or ethically motivated investing can be traced back over 3500 years (Lumberg, 2017)(1)

Thirty years on, the principled positions may have changed but students are no less active in voicing their concerns on social issues such as climate change with the Australian National University’s divestment of fossil fuels being one of many similar examples (Kemp, 2016).

In 2020, this philosophy of socially principled investing has almost become the standard with over 3500 organisations now signatories to the Principles of

Responsible Investing (PRI) collectively representing over USD $100 trillion in assets (PRI, 2020).

Today, our collective thinking in this space has evolved to become a much more sophisticated and ambitions framework. Subsequent sections of this document examine how this collective thinking has evolved and what mechanisms we have to address these issues.

Shift in the behaviour of asset owners and asset managers

Looking back a decade, what we saw was a growing awareness and appreciation of Environmental, Social and Governance (ESG) issues amongst both asset owners and asset managers. Research in this area primarily focussed on the governance element of an individual business as a means of improving returns by biasing towards better managed companies.

Today, that awareness and appreciation for ESG issues has transformed into genuine acceptance and endorsement for the principles of responsible investing. This endorsement is being pushed down from the highest levels of the organisation’s governance structures: senior members of boards and investment committees within these organisations.

So, over the next decade, the executives and investment teams within asset owners will be tasked with executing on the objectives that their governing structures have stated. The next step for many asset managers is to think about how they can help clients address these objectives whilst also delivering a good economic outcome for their underlying members.

Asset owner objectives

Two core principles that drive asset owners as they look to address the responsible investment challenge:

In 2020, this philosophy of socially principled investing has almost become the standard with over 3500 organisations now signatories to the Principles of

Responsible Investing (PRI) collectively representing over USD $100 trillion in assets (PRI, 2020).

Today, our collective thinking in this space has evolved to become a much more sophisticated and ambitions framework. Subsequent sections of this document examine how this collective thinking has evolved and what mechanisms we have to address these issues.

Shift in the behaviour of asset owners and asset managers

Looking back a decade, what we saw was a growing awareness and appreciation of Environmental, Social and Governance (ESG) issues amongst both asset owners and asset managers. Research in this area primarily focussed on the governance element of an individual business as a means of improving returns by biasing towards better managed companies.

Today, that awareness and appreciation for ESG issues has transformed into genuine acceptance and endorsement for the principles of responsible investing. This endorsement is being pushed down from the highest levels of the organisation’s governance structures: senior members of boards and investment committees within these organisations.

So, over the next decade, the executives and investment teams within asset owners will be tasked with executing on the objectives that their governing structures have stated. The next step for many asset managers is to think about how they can help clients address these objectives whilst also delivering a good economic outcome for their underlying members.

Asset owner objectives

Two core principles that drive asset owners as they look to address the responsible investment challenge:

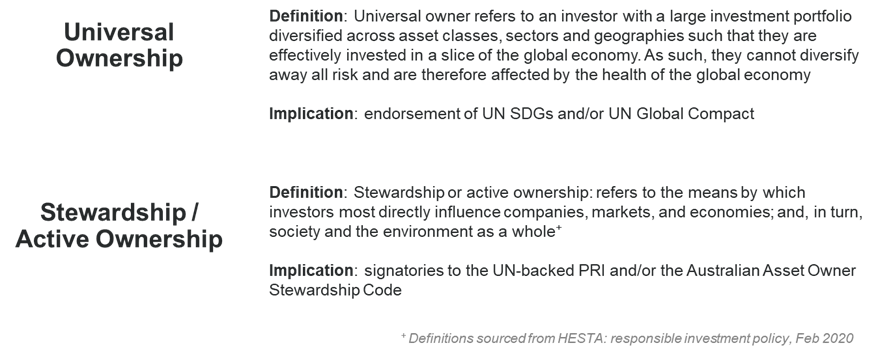

Most asset owners with large diversified portfolios recognise that their obligations as universal owners of assets require them to think about the health of the overall market they operate in in addition to the direct risks their members are exposed to through their investment portfolios. For some organisations, this means endorsing the ambitions of the United Nations Sustainability Development Goals (SDGs). For others, this means looking to integrate the principles of the United Nations (UN) Global Compact.

Independent of which objective they choose to build their responsible investment framework around, asset owners that acknowledge their obligation as universal owners of assets will then need to action their responsibilities as such. In most instances, asset owners have used the Principles of Responsible Investing (PRI) to guide the development of their framework. As signatories to PRI, organisations commit to six principles to assist them in meeting their obligations as asset owners (PRI, 2020):

Independent of which objective they choose to build their responsible investment framework around, asset owners that acknowledge their obligation as universal owners of assets will then need to action their responsibilities as such. In most instances, asset owners have used the Principles of Responsible Investing (PRI) to guide the development of their framework. As signatories to PRI, organisations commit to six principles to assist them in meeting their obligations as asset owners (PRI, 2020):

Investment manager response and scope of Redpoint's framework

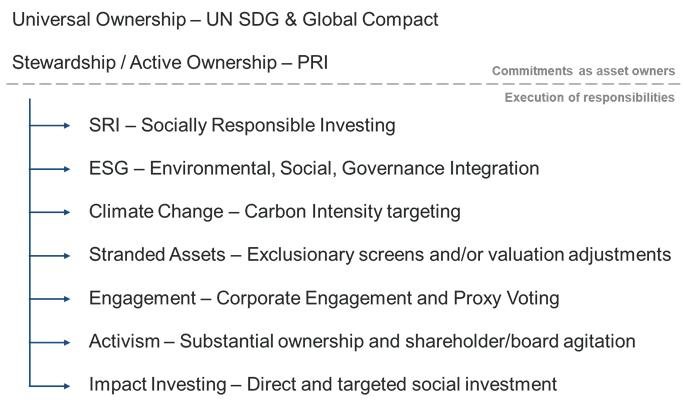

By establishing broader social goals as universal owners (e.g. SDGs) and by creating frameworks for implementation (e.g. PRI), asset owners then need to align these objectives with those of their underlying investment managers who in most cases act as agents in the execution of their overall mandate.

For asset managers, this requires them to establish frameworks for responsible investing that meet the objectives of their asset owner clients whilst also maximising the risk-adjusted returns for their underlying members. In many cases, asset managers also take the onus to become signatories of the PRI reinforcing the alignment between asset owners and managers. This is the case with Redpoint having been a signatory to PRI since our establishment in 2011.

The following diagram highlights the typical areas investment managers focus on to assist asset owners meet their obligations as universal owners: (2)

By establishing broader social goals as universal owners (e.g. SDGs) and by creating frameworks for implementation (e.g. PRI), asset owners then need to align these objectives with those of their underlying investment managers who in most cases act as agents in the execution of their overall mandate.

For asset managers, this requires them to establish frameworks for responsible investing that meet the objectives of their asset owner clients whilst also maximising the risk-adjusted returns for their underlying members. In many cases, asset managers also take the onus to become signatories of the PRI reinforcing the alignment between asset owners and managers. This is the case with Redpoint having been a signatory to PRI since our establishment in 2011.

The following diagram highlights the typical areas investment managers focus on to assist asset owners meet their obligations as universal owners: (2)

Redpoint’s Responsible Investment (RI) framework covers all but two of the above areas (Activism and Impact Investing). The following sections of this document discuss Redpoint’s framework for addressing key investment considerations in relation to these issues.

Redpoint's approach to responsible Investing

Redpoint established its Responsible Investment framework in order to integrate EESG considerations into the equity portfolios we manage on behalf of clients. Our philosophy for the integration of these EESG considerations is focussed on maximising risk-adjusted return. Incorporating exclusions explicitly in the portfolio construction process enables us to address specific Socially Responsible Investment (SRI) principles of our clients in a customised framework. Further incorporation of stock selection disciplines (Alpha) provides greater opportunity to improve risk adjusted returns by selectively allocating capital towards companies with better sustainability characteristics and better medium-term financial prospects.

Hence, our Responsible Investment Framework can be summarised as follows:

Redpoint believe that portfolios need to incorporate all three of the above elements in order to deliver successful investment outcomes and maximise risk-adjusted returns over the long-term. The following diagram provides an overview of the Redpoint Responsible Investment framework.

Redpoint's approach to responsible Investing

Redpoint established its Responsible Investment framework in order to integrate EESG considerations into the equity portfolios we manage on behalf of clients. Our philosophy for the integration of these EESG considerations is focussed on maximising risk-adjusted return. Incorporating exclusions explicitly in the portfolio construction process enables us to address specific Socially Responsible Investment (SRI) principles of our clients in a customised framework. Further incorporation of stock selection disciplines (Alpha) provides greater opportunity to improve risk adjusted returns by selectively allocating capital towards companies with better sustainability characteristics and better medium-term financial prospects.

Hence, our Responsible Investment Framework can be summarised as follows:

- Socially Responsible (SRI) – helps us address the ethical principles of our clients

- Sustainability (ESG) – helps bias our portfolios for long-term good/quality

- Alpha – helps enhance return and manage volatility over the medium term

Redpoint believe that portfolios need to incorporate all three of the above elements in order to deliver successful investment outcomes and maximise risk-adjusted returns over the long-term. The following diagram provides an overview of the Redpoint Responsible Investment framework.

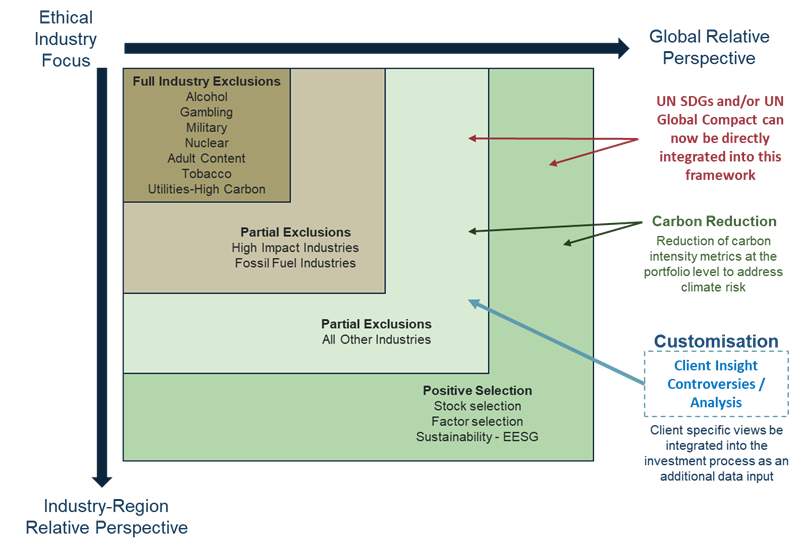

The above framework is used by Redpoint to assist our clients to identify industries and activities they may wish to partially or fully exclude along with identifying opportunities for stock selection from a sustainability perspective.

For Funds or Separately Managed Accounts (SMA), where Redpoint has discretion over product design and portfolio management, Redpoint will exclude investment in companies which have more than 0% revenue exposure to the manufacturing of Tobacco and production of controversial weapons.

Through our Responsible Investment Framework, Redpoint encourages clients to incorporate principles of ESG and/or SRI into an investment portfolio, Redpoint uses multiple perspectives to map client ESG and SRI preferences into quantitative scores that can be used by an optimiser to form risk adjusted portfolios. In turn, the preferred ESG and SRI measures can be incorporated into a quantitative portfolio balanced against other

risk factors and stock selection enhancements to form a broadly diversified portfolio.

This approach essentially translates investor specific ESG and SRI preferences into a customised stock-specific perspective on the quality of a company by examining the firm’s interactions with the broader economy, the environment, society, and the approach to corporate governance. With this insight and design approach, well engineered investments emerge that capture or outperform the benchmark return by holding a broadly diversified set of quality companies, well managed to succeed over the long term.

The framework as presented in the previous figure highlights that both exclusionary principles as well as positive selection can be incorporated to address the specific ethical SRI and ESG considerations of our clients. Ethical considerations allow clients to exclude stocks in the alcohol, gambling, military, adult content, and/or tobacco industries. For ethical reasons, utility firms with high carbon intensity and/or nuclear activity may also be excluded.

ESG considerations are then applied to the rest of the market and can be used to exclude specific stocks, such as in high impact (chemicals, metals, mining, paper, pulp) and fossil fuel industries. In all other industries, stocks can be excluded based on extreme negative ESG considerations. Positive stock selection using both ESG/Carbon intensity considerations as well quantitative factor selection allows for the better re-allocation of capital released from the negative screening process.

Redpoint's approach to EESG

ESG investing considers a firm’s environmental, social and governance (ESG) policies. Favourable ESG policies focus on all stakeholders who have a role in a firm’s success. Stakeholders include management, labour, the environment and society at large in addition to shareholders.

A stakeholder focus is at odds with traditional economic theory. According to traditional theory, managers act as “agents for shareholders” and should manage the firm to maximise profit to enhance shareholder returns. In contrast, many “management best practices” consistent with maximising profit recommend focusing on the interests of all stakeholders. A firm managed with all stakeholders in mind will often spend money for projects without obvious, immediate benefits for shareholders. A natural question for investors to ask is are expenditures on employee benefits and the environment harming shareholder wealth or do these activities build employee and brand loyalty helping to make firms more efficient and durable for all economic conditions?

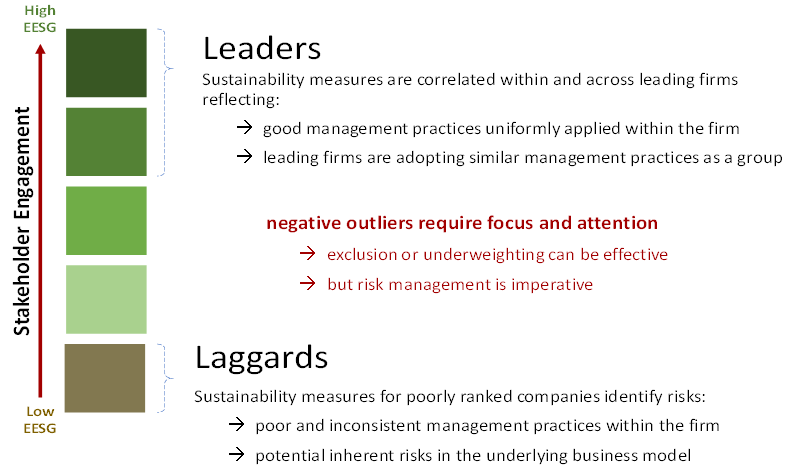

Like many investors, Redpoint sees value in a stakeholder view of the firm to maximise profits and return for investors. Incorporating a stakeholder perspective by embedding EESG metrics into our investment process allows us to identify those companies that are seen as ‘leaders’ of industry. These companies exhibit good management practices uniformly applied within their organisation and are consistently maintaining or improving their processes towards best practice standards relative to their peers. Often, many of these firms would have grown successfully over time through the establishment of good management practices.

This stakeholder perspective also allows us to identify those companies that may be lagging their peer group in terms of managing their companies for long term success. These companies tend to be negative outliers and warrant further focus and attention. Often, these companies do not consistently apply standards of best practice across their organisation to manage EESG issues, or they have a potential EESG risk embedded in their business model that warrants a discount in valuation.

Incorporating this stakeholder perspective allows is to distinguish among firms based on ESG considerations to identify ESG “Leaders” and ESG “Laggards” as outlined below.

For Funds or Separately Managed Accounts (SMA), where Redpoint has discretion over product design and portfolio management, Redpoint will exclude investment in companies which have more than 0% revenue exposure to the manufacturing of Tobacco and production of controversial weapons.

Through our Responsible Investment Framework, Redpoint encourages clients to incorporate principles of ESG and/or SRI into an investment portfolio, Redpoint uses multiple perspectives to map client ESG and SRI preferences into quantitative scores that can be used by an optimiser to form risk adjusted portfolios. In turn, the preferred ESG and SRI measures can be incorporated into a quantitative portfolio balanced against other

risk factors and stock selection enhancements to form a broadly diversified portfolio.

This approach essentially translates investor specific ESG and SRI preferences into a customised stock-specific perspective on the quality of a company by examining the firm’s interactions with the broader economy, the environment, society, and the approach to corporate governance. With this insight and design approach, well engineered investments emerge that capture or outperform the benchmark return by holding a broadly diversified set of quality companies, well managed to succeed over the long term.

The framework as presented in the previous figure highlights that both exclusionary principles as well as positive selection can be incorporated to address the specific ethical SRI and ESG considerations of our clients. Ethical considerations allow clients to exclude stocks in the alcohol, gambling, military, adult content, and/or tobacco industries. For ethical reasons, utility firms with high carbon intensity and/or nuclear activity may also be excluded.

ESG considerations are then applied to the rest of the market and can be used to exclude specific stocks, such as in high impact (chemicals, metals, mining, paper, pulp) and fossil fuel industries. In all other industries, stocks can be excluded based on extreme negative ESG considerations. Positive stock selection using both ESG/Carbon intensity considerations as well quantitative factor selection allows for the better re-allocation of capital released from the negative screening process.

Redpoint's approach to EESG

ESG investing considers a firm’s environmental, social and governance (ESG) policies. Favourable ESG policies focus on all stakeholders who have a role in a firm’s success. Stakeholders include management, labour, the environment and society at large in addition to shareholders.

A stakeholder focus is at odds with traditional economic theory. According to traditional theory, managers act as “agents for shareholders” and should manage the firm to maximise profit to enhance shareholder returns. In contrast, many “management best practices” consistent with maximising profit recommend focusing on the interests of all stakeholders. A firm managed with all stakeholders in mind will often spend money for projects without obvious, immediate benefits for shareholders. A natural question for investors to ask is are expenditures on employee benefits and the environment harming shareholder wealth or do these activities build employee and brand loyalty helping to make firms more efficient and durable for all economic conditions?

Like many investors, Redpoint sees value in a stakeholder view of the firm to maximise profits and return for investors. Incorporating a stakeholder perspective by embedding EESG metrics into our investment process allows us to identify those companies that are seen as ‘leaders’ of industry. These companies exhibit good management practices uniformly applied within their organisation and are consistently maintaining or improving their processes towards best practice standards relative to their peers. Often, many of these firms would have grown successfully over time through the establishment of good management practices.

This stakeholder perspective also allows us to identify those companies that may be lagging their peer group in terms of managing their companies for long term success. These companies tend to be negative outliers and warrant further focus and attention. Often, these companies do not consistently apply standards of best practice across their organisation to manage EESG issues, or they have a potential EESG risk embedded in their business model that warrants a discount in valuation.

Incorporating this stakeholder perspective allows is to distinguish among firms based on ESG considerations to identify ESG “Leaders” and ESG “Laggards” as outlined below.

By screening to underweight or to exclude firms with poor sustainability, a broadly diversified global portfolio can be formed without sacrificing performance or increasing volatility relative to a market benchmark. This approach extends traditional notions of corporate engagement to a broad range of global companies.

Incorporating positive stock selection through ESG, carbon intensity or quantitative factor selection allows for the better re-allocation of capital released from the negative screening process.

Conclusion

Redpoint has been integrating EESG considerations into our portfolios since the inception of our organisation. We built and continue to develop our proprietary EESG rating system, the Redpoint Rating, which translates these important EESG considerations into stock level perspectives of company quality. We believe these considerations will become increasingly important given the shifts in investor behaviour over the last 10 years with a much greater focus on the management practices of the companies they invest in.

Institutional clients also continue to evolve their approach to responsible investing with a significant build out of philosophy and policy. This evolution in thinking has resulted in a greater recognition of institutional client’s responsibilities as universal owners which they are looking to address through global endorsement of United Nations backed initiatives, such as the Sustainable Development Goals (SDGs) & Global Compact. In addition, institutional clients increasing activity to address their responsibilities as universal owners by endorsing the PRI’s principles of Stewardship and Active Ownership.

Redpoint’s Responsible Investment framework aims to complement these objectives by:

Incorporating all three elements allows us to maximise risk-adjusted returns and deliver successful investment outcomes for our clients over the long-term.

(1) Note that this is a representative history not a precise history. Full reference is provided in the bibliography

(2) Note that this is an indicative, not a comprehensive list

Incorporating positive stock selection through ESG, carbon intensity or quantitative factor selection allows for the better re-allocation of capital released from the negative screening process.

Conclusion

Redpoint has been integrating EESG considerations into our portfolios since the inception of our organisation. We built and continue to develop our proprietary EESG rating system, the Redpoint Rating, which translates these important EESG considerations into stock level perspectives of company quality. We believe these considerations will become increasingly important given the shifts in investor behaviour over the last 10 years with a much greater focus on the management practices of the companies they invest in.

Institutional clients also continue to evolve their approach to responsible investing with a significant build out of philosophy and policy. This evolution in thinking has resulted in a greater recognition of institutional client’s responsibilities as universal owners which they are looking to address through global endorsement of United Nations backed initiatives, such as the Sustainable Development Goals (SDGs) & Global Compact. In addition, institutional clients increasing activity to address their responsibilities as universal owners by endorsing the PRI’s principles of Stewardship and Active Ownership.

Redpoint’s Responsible Investment framework aims to complement these objectives by:

- addressing the ethical challenges of our clients through our socially responsible SRI screens,

- biasing for long-term quality through our EESG sustainability rating system, and

- enhancing return and managing volatility over the medium term using our proprietary alpha models.

Incorporating all three elements allows us to maximise risk-adjusted returns and deliver successful investment outcomes for our clients over the long-term.

(1) Note that this is a representative history not a precise history. Full reference is provided in the bibliography

(2) Note that this is an indicative, not a comprehensive list

Important information : This communication is provided by Redpoint Investment Management Pty Limited (ABN 83 152 313 758, AFSL 411671) (Redpoint). The information in the communication is of a general nature only and is not financial product advice. The communication is not intended to offer products or services provided by Redpoint or its affiliates. Opinions constitute our judgement at the time of issue and are subject to change. Neither Redpoint nor its employees or directors give any warranty of accuracy or reliability, nor accept any responsibility for errors or omissions in this communication.